Tommaso Di Bartolo is a serial-entrepreneur with 2 exits, author, advisor & angel investor and lives with his family in Silicon Valley.

As an entrepreneur, you’ve probably dealt with your fair share of failure. It’s the name of the game, and often inevitable. However, there is an attribute that is completely in your control that you are capable of honing. What is this attribute that can mean the difference between failure and success? Hustle. But if you’re not a natural one, how can you mold yourself into being a great hustler?

When you hear the word hustler (especially outside Silicon Valley) does it bring negative connotations to mind? You might picture a guy in a dark pool hall downplaying his skills until he puts up a large bet and suddenly flaunts his talent, hustling his opponents. There are a number of negative images of hustling like drug dealers, rigged carnival games, or street vendors selling illegal goods.

Yes, all of these situations are examples of hustling, but … hard-working people are hustlers, too. Hustling, depending on your means and motivation, isn’t always a bad thing.

Your Startup Needs a Hustler

In fact, in terms of your startup’s success, I want you to think of hustling as a great thing. Think of athletes sacrificing their bodies to make the tough play or putting in endless hours at the gym to improve their game.

Hustlers go all out every day, pushing past their breaking point. Even when they are exhausted, hustlers never quit doing the hard work, putting in the long hours others won’t. Hustlers always work to better themselves, and the hustle is what separates the champions from the losers.

Hustling is an art form

It’s earning or making something from seemingly nothing by maintaining the mindset of a go-getter. While hustling gets a bad rap from the criminal acts it’s often associated with, it’s not a crime. Hustlers don’t wait for success to come to them; they go out and get it for themselves.

In entrepreneurship, hustling means doing whatever it takes, legally, for your startup to be successful. If you’re not sure how to start honing your hustler status, start by following these ten practices.

1. Never Lean Back

A hustler always pursues progress and constantly works to get things done. One way to learn to become better than you currently are is by setting bold goals. Set goals that are uncertain and a little scary. An uncertain goal might not work out, but working toward something that is not a foregone conclusion is all part of the hustle. Setting an audacious goal and doing everything you can to make sure it gets reached is a sign of a true hustler.

By never leaning back, you aren’t tempted to halt your pursuit of perfection. It’s not so much about feeling like you never have enough as it is about working to improve yourself and your startup everyday.

2. Promote Yourself

Self-promotion is a necessary part of being a hustler. There is a balance to find in this hustle between complete humbleness and being a jerk in self-promotion. While you don’t need to plaster your social media and blog with personal accolades, you do need to be dedicated to promoting your startup by telling people what you are up to.

You’ll want to show confidence in your startup’s successes. It’s hard to hustle in something you don’t believe in, so don’t be afraid of self-promoting and showing your belief in yourself and your startup.

4. Don’t Fear The Critics

Putting yourself out there is a risk. Be ready for haters and don’t let them slow you down. One characteristic of hustlers is their ability to brush off criticism and rejection without getting embarrassed or upset. In fact, you need to be completely indifferent to the haters.

As a hustler, you have to answer even negative emails, respond to harsh critics, and make sales pitches to investors who seem less than interested. It’s all part of doing everything you can to make your startup work. No matter what you do, you’re going to have to deal with critics, but if you want your startup to be successful, you have to ignore the haters.

While you might find it easy to ignore the critics when they are practically strangers, sometimes the critiques come from the people we love and trust like our family and friends. They may not understand why you are doing what you’re doing, and they may not share your vision — and they don’t have to. However, this can be a difficult situation, since you likely care about what they think of you, and you may even find yourself giving in to their point of view. As hard as it is, you have to move past them as well.

Hustlers are able to ignore negative feedback, bad advice, and even criticism from loved ones. As a hustler, you should be so busy doing the work it takes to be successful that you don’t have time to be worried about how other people, both strangers and family, view you.

5. Make Connections

The saying “It’s all about who you know,” holds a lot of truth in relation to startups. As a hustler, you need to make connections with many people in many industries to get your startup out there and help ensure its success. By nature, hustlers tend to be very social, which is beneficial to the business aspect of your startup.

While you can use your connections to sell your product or service, don’t forget that some give needs to accompany the take. Use your connections as your go-to source for buying what you need for your startup, and the symbiotic relationships will benefit everyone involved.

As an entrepreneur, you can’t be the type of hustler that just shakes people down for what you need. Understand how to treat people well, be genuine in your relationships, and treat your connections fairly.

6. Take What You Need

If you can’t get what you need, you might be forced to take it. That’s essentially the main characteristic of a hustler: going out and getting what they need. However, in the startup world, it’s going to be a little more difficult than just grabbing and going. It will likely take a lot of hard work. You might need to ask friends and family for help or even make cold calls.

7. Show What You’ve Got

People should know what you’re capable of and fear your potential, but do it in a way that keeps you approachable. Be aware of the situation and know when is the right time to use your killer instinct.

8. Carry Yourself with Confidence

Yes, the fact that you are working for the success of a startup means you probably haven’t been in the game for long. However, you should carry yourself like you’ve been at it for years. Showing confidence is especially important for making good first impressions. Carry yourself well and dress to impress to let people know you are ready to hustle.

Even if you know you might not be the best man for the job, others don’t need to know it as well. Conduct yourself with confidence without being overly cocky. As a hustler, you need to be confident in dealing with others, and you will likely have to take charge of the situation to make sure things get done.

Don’t be afraid to be the Alpha and control the outcomes of certain situations and meetings.

9. Hone Your Street Smarts

You may have been a star student, but out in the real world, you need more than book smarts. As a hustler, you need to have street smarts as well. Trying to run a successful startup means you’re going to be faced with many unexpected situations and challenges.

Many of these situations will require quick decisions and reactions to keep your startup successful. You will begin to have quicker reactions — which rely heavily on street smarts. By taking the time and the challenge to hone those skills, you will be much better at reacting to those unscripted moments — which is another mark of a great hustler.

10. Never Make Excuses

If you want to be a great hustler, you are not going to be able to let off the gas; you will have to outwork everyone else. A successful startup requires much more than a nine to five schedule. Prepare to burn the midnight oil in order to see your startup be successful.

We mentioned at the start that talent and luck are typically out of your control. However, you might find that as you work harder and hustle more, your luck starts to improve, and you learn to work smarter.

Even if you become a great hustler, you’re not guaranteed to be faced with failure. If you do fail, take responsibility for it. You are hustling for one purpose, and that purpose is to have a successful startup. Failure should not be an option and you definitely shouldn’t make any excuses for your failure.

TAKEAWAY

Maintain the mindset of a hustler at all times. Be obsessed with it, do whatever it takes, and believe in what you are offering. If you’re not obsessed with becoming a great hustler, then you will never truly be one. It’s hard to hustle for something you don’t believe in, so believe in your product or service and its ability to solve the consumer’s problem.

In order to be a great hustler, you need to enjoy doing it, even when it gets hard. By believing in and enjoying what you are doing, it makes it that much easier to get up every day and hustle even harder to reach your goals and startup success.

Originally published at www.startupgrind.com.

A startup I advise was facing challenges with the VC intros they were getting. They were disrupting the Brazilian fishing industry with a VR/AR app that expedited the phase of finding where fishing boats should drop their nets - but when it came to fundraising, the fish weren’t biting. Once in Silicon Valley, they were introduced to four venture Bay Area firms. As a response to the intro, the founders attached a NDA for the investor to sign in preparation of their meeting.

Obviously, 4 out of 4 didn’t respond.

In our conversation — we didn’t just expand upon do’s and don’ts, but also on how to bond with investors as they turn into business partners. Two months into fundraising and couple lessons learned later, they raised their round.

As a startup founder, you either have a tendency to give away too much information with investors, or you belong to those founders that are overly cautious and don’t tell investors enough. Before you head into your first meeting with investors, it’s important to know what you are going to divulge and what you are going to hold back. But how do you know what information you should share with VC’s?

Being transparent helps earn the trust of others, and it can help you avoid having to keep track of any partial truths you’ve told. However, before you reach the due diligence phase with investors, you do want to hold some things back in your first meetings. Similar to dating, you want to take things one step at a time. You don’t want to spill all of your secrets on the first date, but rather create some excitement.

Whether you are prone to sharing every secret or keeping most things locked up, it’s important to find a balance between the two extremes. The balance between the two extremes is delicate. For first meetings, it’s wise to keep discussions limited until you understand if this VC invests in your space and that your startup sounds interesting, and then open up more in those meetings.

Rather than schedule countless first meetings with VCs, limit the number you see when you are beginning your fund raising process. For one, word gets around in the investor circles, and if investors hear that your startup has been passed on multiple times, people will hear, and your startup will look over-shopped and lacking momentum.

Second, information about your startup can leak in conversations. In fact, once VCs have picked a startup to fund, they often share what they’ve learned about the competition to the one they choose. It is something to think about when you consider what to disclose in meetings with VCs. Be thoughtful of what information you will be comfortable with one of your competitors having.

Don’t let the thought of your competitors receiving information about your startup make you overly guarded. It will be an immediate turn off to VCs, and they may even wonder why you met with them in the first place. You are looking for someone to partner with your startup, so by denying answers to any straightforward business questions, you won’t be able to build trust with potential investors.

Not sure what business information to share? Use your past performance as a talking point.You can keep the discussion serious and financial projections high-level without divulging any of your sensitive plans. There shouldn’t be anything in your past performance that would impact your ability to move forward, so don’t keep that area private.

Guard Your Future Strategy

The information is likely proprietary, and the competition will want to know where you are headed, so don’t completely let on to what your future strategy is. That’s not to say you shouldn’t share any strategy with VCs. That would make you seem unplanned and not give them anything of interest to focus on. Instead, guard the parts of your future strategy you feel are sensitive. Additionally, don’t hint towards any strategies or plans that you won’t fully talk about. This makes you look and sound cagey and is a turnoff to VCs. Leave them completely out of the conversation, and don’t even allude to them.

Your potential investors will likely want to know about your current customers. If you show them a list of your key customers or partners, and if you don’t want them to be contacted, be sure to make that clear. Let them know that, if things move forward, you will organize calls with your customers. If you are very serious about protecting your customers, you could even casually state that if they are contacted, it could affect which VC you decide to work with. Be careful with any ultimatums, though, if you are raising funds early on, as you won’t have much traction to make demands.

As VCs start to show more interest and has taken two or more meetings, they may start to ask you for more information. Be ready to share your past 12-month financial performance and your future forecasts. It is an appropriate time for VCs to ask for this information, and if you are not ready to share that information, you may not be ready for funding.

If you are becoming more comfortable with a potential investor and could imagine working with them, you can start to slowly reveal more of your future strategy. Ask VCs to debate your strategy with you, as that will give you an excellent idea if you would work well together. Your VC will be your “partner”, so it is important to know how they debate your strategy.

Give potential investors confidence with the information you provide. For example, if they request a certain type of analysis, use it as an opportunity to show them how thorough and efficient you can be by answering their question with a professionally produced material.

At this point, if your potential investor looks like they will be a good partner, it is probably a good time to allow some customer calls. Carefully choose which business partners or customers you allow them to call. You will essentially be arming them with ammunition to use with their partners before and after your meeting.

As you get further along in the process, expect the questions to become more intrusive. More customer calls will be made, future strategy will be discussed, and the financial model will be dissected and potentially redone. At this point, you should disclose any major issues that would seem deceptive to share after the term sheet. Major issues can include:

For the most part, major disclosures can be overcome if they are shared in the right way and at the right time. Anything that would make you look shady or distrustful if revealed after your potential investor asks for final approval should be disclosed. If you hold something back that comes out later, your potential investor could drop you rather than go back to their partners and tell them what you disclosed.

Before you reach final due diligence and submit a term sheet, there are certain areas of information that would be wise to protect for your startup. You should be completely honest with your answers, but you don’t want to reveal certain sensitive areas until funding seems imminent.

Full financial model

Early on, a high-level profit and loss summary is enough for potential investors. You may need something more detailed if you are involved in a merge or acquisition, but you shouldn’t have to share exactly how operations work. Be practical in the metrics you give. Using excessive metrics can lead to unnecessary discussions that don’t matter at an early stage.

Don’t write sensitive information

Anything you don’t want given to your competitors should not be written down. You may have to share some sensitive information, but only do it orally, not in writing. VCs can’t remember anything and can’t note everything down, so it’s best to keep it verbal.

Operational problems

When you reach the due diligence stage and are turning in a term sheet, then you should divulge this information. But, early on, as you are just trying to raise interest, keep issues with operations, personnel, platform, etc. quiet.

Detailed customer list

If they do request a customer list early on, you could keep it anonymous by naming customers by letter, like Customer A and Customer B.

Valuation

As a startup, you should avoid discussing valuation when you are first meeting with potential investors. If you are asked, don’t be specific so you can avoid either over or under valuing your startup. Investors may take advantage of you if you undervalue your startup and fund you at that valuation or lower.

VCs aren’t trying to cheat you, but they are trying to maximize their own return.

If you overvalue your startup, VCs may not bother with you at all, and you could miss out on funding by being overly optimistic with your valuation. A valuation that is too high or too low can be a red flag to potential investors. They may think that you don’t fully understand or are not ready for fund raising or the value of your startup. Since word gets around, it could be detrimental to your reputation as a startup founder and negatively impact your fund raising goals.

As you meet with VCs and try to raise funds for your startup, the question becomes less of how much information you share and more a question of when you share certain information.Very few of the potential investors you talk to will partner with you, and once it is apparent they will champion for your cause, you need to be fully transparent with them.

If an investor doesn’t fund you, they may become competition and share your information, either directly or indirectly. They aren’t actively trying to sabotage you; it is just their job to get information from you, whether or not they invest.

There are two main factors to consider when deciding how much information to include in your answers to potential investors:

As a startup, raising funds is an essential part of the job. However, don’t go into meetings with potential investors until you are ready to be funded and answer the questions they may have about your startup. Be prepared to be open, but know that there are areas where you can draw the line. Generally, however, you will want to be an open book to VCs.

The trust relationship between startups and investors is essential to the partnership. Unless your startup is dealing with a never-before-seen, patentable technology and showing the technology will require you to file a patent right away, you should answer nearly all of your potential investor’s questions to some capacity. By doing so, it will be easier for you to get invaluable advice, find the investors that fit with your startup, and meet your funding goals.

If you are honest with VCs, the time consuming and stressful process of raising funds can help you gain new relationships beneficial to the future of your startup, whether or not they fund you.

By Tommaso Di Bartolo for Startup Grind

Startups take a lot of hard work, dedication, and sacrifices to make it happen. Even then, your dream doesn’t always pan out in the real world. Maybe you were able to make your startup work for a while, but the reality of what it takes to sustain it is too much for you and your team. Or, maybe your success was short-lived, and now your startup has lost steam and isn’t doing well. Whatever the reason may be, consider building your startup from the beginning ready to be acquired. But how do you make your startup desirable to buyers?

As a startup, you might not have had the time to dedicate to administrative-type tasks like bookkeeping and contracts. In the beginning, there’s not much to be organized anyway. However, a lack of organization looks messy to outside buyers. While it works for you in this stage, it can instill doubt in potential buyers. Don’t make things hard for potential buyers by leaving things a mess but structure early on the following things:

BOOKS: make sure all of your expenses are organized and entered, bills are up-to-date, bank accounts are balanced, and your finances records are in order.

CONTACTS: If your contract data is not easily accessible and organized, it is essentially useless to potential buyers

IP: Have a system in place to define your private and public IP addresses and how they are allocated amongst locations, subnets, users, etc.

CAP TABLE: Simplified, your cap table should tell potential buyers who owns what. You can have holders grouped into simplified buckets called “founders” and “investors.” You could even include formulas that map out the hypothetical sale of your startup. Not only will it impress buyers, but having an updated and organized cap table allows you to make good decisions quickly.

Use the tools at your disposal to get organized. Cloud-based tools allow you to save and share documents with potential buyers, and many of them are free to use. Consider taking advantage of Google Drive, Box, or Dropbox to keep your startup’s information organized into folders. Not only will this make the due diligence process much faster, it will impress potential buyers.

The quickest way for you to reduce the valuation of your startup is by actively seeking a buyer. In fact, there is a ten-times or more valuation difference between you approaching a buyer and a buyer approaching you. Additionally, if you are selling non-stop, you’ll start to look desperate to potential buyers.

If you want to get the best valuation for your startup, you need to be convincing about its growth opportunity. If you use your existing operating performance, or EBITDA, you’ll only get a valuation based on the now. However, if you can be convincing about the potential of your startup, it is possible you will be able to sell for a much higher valuation.

When you have a potential buyer, think about how your startup can do for them and create a product integration plan for post-acquisition. Show the buyer what your startup can do for their company in the next five years before they make an investment to prove your potential.

Identify potential buyers early. And by early, I mean at least 18 months in advance. When you make that list of all of your potential buyers, start building relationships with them. When it comes time to sell, you’ll have multiple potential buyers who are interested in your startup.

Start by talking to potential buyers about a partnership or alliance. Having an existing business relationship with the buyer can lead to a strong and stable outcome.

If you have friends within a company you could sell to, see if they can coordinate introductions with high-level managers. Don’t waste too much time talking to people within companies who do not have the decision making power required to acquire your startup.

Be upfront about the fact that you are selling your company, but don’t be all sales all the time. The saying goes, “Ask for money, you get advice; ask for advice, you get money,” and it does apply to the sale of your startup.

Have ongoing conversations with potential buyers about ways you can work together. This is the best way to drum up offers. You might have to work your way up the ladder with your conversations and have them with many different people before you get to a decision maker who is high-up enough to make you an offer. You must convince that person that buying your startup is a better idea than partnering with it.

Get your team on the same page with your valuation and what will go and stay with the startup. There will likely be valuation parameters and other things to discuss. Will everyone be satisfied if the buyer shuts down the product? What will you do if the buyer won’t take all of the current employees? Will the company allow your startup to run independently? Consider these important questions with your co-founders and make suree everyone is on the same page before you start the acquisition process.

Understand you might not get premium, even if you think you deserve it. In most startup cases where deal sizes vary from $5M-$20M acquisition prices, founder teams are out for being acquired because they managed it up to a certain point but can’t move ahead. In all likelihood, business has stalled or you’ve lost your drive and are ready to move on. Taking these factors into consideration, realistically, you won’t get a premium valuation. Save time and protect yourself by taking the time to understand the market and having realistic expectations. Of course, you will feel like you deserve premium considering how much time, effort, and money you’ve put into the startup and how many sacrifices you’ve made. However, this won’t make a difference to buyers, and sometimes you have to accept that getting something is better than getting nothing.

Understand how investors will value your startup. It’ll be by either your financial value or your strategic value, and it will mainly depend on your revenue and model of your future cash flow. In tech, however, it’s likely you’ll be valued based on how you fit in with the buyer’s future strategy. Some things that could give you strategic value are:

There is no “right” price for your startup, so your price depends on what you can negotiate based on what metrics the buyer’s team uses to justify a price. Keep in mind that the first offer is rarely the best offer, so don’t be afraid to say no and counteroffer.

A Startup is NEVER in sale because business is great — but be always open to chat! Hence sell only when you are ready. Negotiating a sale is incredibly time consuming and distracting for your startup, even more so than raising money. You’ll have to cease running day-to-day operations as you pursue an acquisition, so only start the process if you definitely want to sell the startup, and you’re likely to get a price you are willing to accept. Don’t waste your time or efforts talking to potential buyers just out of curiosity. However, don’t wait too long to sell if things start to stagnate. You are much less likely to get an acceptable offer if you wait until things get too far downhill.

Take advantage of multiple options. The best time to sell is when you have options, and they are not necessarily all acquisition offers. You could have options of venture term sheets for your next round. You might be in the position to turn down offers if you are operating profitably and buyers are looking to absorb the competition.

As a team, agree upon a sell-by deadline. This is not a date that everything has to be finalized. It is just a date by which an offer needs to be accepted by. Consider giving yourself a quick deadline, like 30 to 60 days. Not only will this motivate you every day and give you something concrete to pursue, it will limit the amount of time and energy you spend on pursuing an acquisition. A deadline will help you weed out buyers who are not genuinely serious about your startup.

TAKEAWAY

Regardless of how passionate and dedicated you were to your startup, build your path in a way that you are always ready to be acquired — as you don’t know what you don’t know. Whether progress has stalled or you’ve just lost your drive, there are always options and a path to exit. Perhaps you haven’t considered being acquired yet, and you were approached with tempting offers because of your success. Whatever the reason, worst thing that can happen is that such a situation comes up and it catches you off guard — which leaves you with no time to run the process, or eventually with less key players in your team which would raise the valuation.

By Tommaso Di Bartolo for Startup Grind

Business valuation of any kind is never cut and dry. For startups with little or no revenue and an uncertain future, assigning a valuation is especially tricky. For mature businesses that are publicly listed and have a steady revenue, there are specific facts and figures to use to determine a value. However, a startup is much more difficult to value since it is likely nowhere near making relevant sales. If you need to raise capital for your startup, it’s important to determine what your startup’s value is. But do how to best value your startup?

A startup in the BI space I mentored in 2013, found themselves in some hot water with their funding strategy, which started out when they determined their series A valuation. They thought that it would be better to value their startup aggressively, rather than modest. Now, while they ended up raising $5 million at a $25 million post-valuation, when raising their Series B round, because their poor growth rate they had to raise at a down round of $15 million. Outch! The lesson learned was expensive for all involved parties — and their funding evolution was hit by a major draw back which caused also one of the founder to step out of the venture.

It’s been said that valuing a company is more of an art form than a science. This is even more true for valuing startups that have much less data to work off of. In short, your startup is worth what someone is willing to pay for it.However, it is possible to master the art form and assign a value to your startup that both makes sense to you and is in line with investors’ expectations.

Approach investors with financial forecasts. While it’s decidedly difficult to forecast a startup’s revenue, you will need to have some idea of financial projections to determine value and to defend your value to investors. Step into the shoes of potential investors to understand the importance of this step. You need to get them excited about investing in your startup instead of the hundreds of other startups they see throughout the year. Investors are searching for their next 10-times return startup opportunity. Your five-year financial forecasts should show growth that can afford them that return.

Do your research. You can value your company, even in the earliest startup phases, by looking at similar companies in your industry and geographic location and their valuations. This will give you an idea of the potential you have in your market. You may see a multi-million dollar potential to your business idea, but your investors will need to be convinced of your potential and your startup’s worth. Knowing the comparables will give you a leg to stand on in defending your valuation.

To find out how much other businesses in your industry are selling for, you can use resources like BizBuySell or BizQuest. Additionally, accountants and lawyers make excellent advisors to help you determine the value of comparable startups at your stage. Be sure to talk to both, as one tends to overvalue and the other tends to undervalue startups.

Pick a financial advisor’s brain. If you are struggling with the research portion and you are having trouble finding the relevant valuation statistics for your industry, a financial advisor can assist you. Ask them to help you find valuations determined in recent financings, or recent M&A transactions in your market.

Investors and Startups both need to know the value. Having solid support of your value is important when it comes to raising capital. You will not be able to raise money from investors if you don’t know at what value you are raising funds. So do your homeworks before meeting investors.

One of the most basic economic principles is that of supply and demand. You can use this principle for valuing your startup. As the name implies, the more scarce a supply, the higher the demand. For your startup, that means if you are part of a much-talked about new patented technology startup, you could drive up your valuation by attracting multiple interested investors competing for the deal.

Most startups won’t be fortunate enough to experience multiple investors courting them for a deal. However, even if you don’t have real demand from investors, you can create a perceived demand when dealing with one investor. To do so, don’t let them think that they are the only investor interested in your startup, as that can decrease your valuation. Work to portray your startup as new and unique to create the scarcity needed to maximize your valuation.

The market determines your value. You might have a number in your head for what you think your startup is worth. When you go to investors, though, they might give you a different number. For example, while you think that $5 million is a fair valuation based on liquid assets or receivables, investors are telling you that your startup is worth $1 million. If you are unable to raise capital with a higher valuation, even if you are worth more, you will have to accept your value at what the market says it is.

On the flip side, if you raise money from friends or family rather than professional investors, it’s likely that your startup is overvalued. Your father or old roommate might be willing to pay $20 per share, but future investors may not pay more than that, even as you grow.

You can influence the number the market puts on you. While this may seem contradictory to the previous point, you do have some influence in your market value. You’ve likely given investors a reason to believe your startup is only worth $1 million rather than $5 million. Find a way to value your company on something other than historical performance, since you don’t have a history yet. Use comparables and financial projections to raise your valuation.

Since you likely haven’t made a profit, look to the future for value.Without a history showing profit or revenue, your startup has very little to no liquidity. Without cash flow, it is difficult for startups to determine their valuation. It’s going to take time to become profitable, so you will need to look to your future success to determine a value. Ask yourself a few key questions:

A company may be worth a fraction of the number they are valued at when they reach profitability. Factors like likelihood of success and the quality of the management team should be taken into factor.

Your industry makes a difference. Each industry has its own way of valuing startups. For example, an VR/AR Startup would have a much higher valuation than a SaaS CRM. Research the valuations achieved in recent investments or M&A transactions in your market before you approach investors.

Some angel investors and venture capitalists use a “rule of thumb” value to quickly come up with a range of startup value. The values are typically set by the investors, and they depend on the startup’s stage of development.Simply put, the further along the startup has progressed, the lower the investor’s risk and the higher its value. Examples of stages of development include:

What Grade Are You? Another way to look at the developmental stages is by breaking it out into four stages similar to the four years of high school education. The stage you are in is a key factor in determining your value.

Investors will be much more open to your valuation expectations if you can be specific on why you need the funding and how you will use it. Unless you are ready to back up a high valuation with growth potential, and you are ready for the roller coaster ride, stick to a modest valuation.

One way to prove your value to investors is by testing your idea out a few times. Get enough results that you can show to potential investors and prove that, with some investment, you have something to offer the industry and can grow and meet expectations. If someone is going to give you money, it is important to them that they can see that your idea works and they will earn a return on their money.

Be upfront about your plants, whether you are looking to go all way through or you plan to exit with the first opportunity. It’s important for investors to understand your mentality.

THE TAKEAWAY

Compare your venture assets such as team, KPIs and IP to other players on the market — and understand at how much the competitive landscape raised. Sites such as Crunchbase and CB Insights are of great help to do so. While it is tempting to give your startup the highest valuation, remember that you will need to meet the growth expectations to stay at a high valuation. Hence, if you are unrealistically high on your valuation, it could make your startup life difficult down the road.

Follow Tommaso’s blog on What It Takes.

By Tommaso Di Bartolo for Startup Grind

You’ve likely heard that there are only six degrees of separation between you and anyone else on the planet. When it comes to your startup, it’s vital to make connections and regardless of how many people it takes to get you to the right person, no one is too far removed. If you enjoy networking and connecting, it can even be enjoyable to facilitate those connections. However, not everyone has stellar networking skills right off the bat. Becoming a better networker is critical to your startup, and it could even be the key to your startup’s success. But how to mingle and network like a boss?

One afternoon I was standing at Venetia in Palo Alto enjoying a post-lunch espresso as I often use to do. The bar was pretty quiet, but there was another man there that was standing at the bar sipping his cappuccino. We struck up a conversation, and the typical small talk question of “What do you do?” popped up. He told me that he was creating an AI tool for parents to come up with suggestions based on their kids’ moods, preferences, and behaviors.

At the end of his description, we continued to talk, and he asked me more about myself and showed a genuine interest. We traded business cards at the end, and he made it a point to send an email that same day letting me know that he enjoyed our conversation. I was impressed with both his startup and his networking skills, and — to make a long story short — I ended up investing as an angel investor. Of course, he was in the right place at the right time, but had it not been for his networking skills and willingness to put himself out there, I would have not invested in his startup.

You can ease your way into networking by starting with coffee meetings. If you commit to one meeting a week over the course of a year, you’ll have 50 meetings. Here are some tips to take into those meetings.

If it’s your first go around with networking, you’re likely to make some mistakes. Here are some mistakes you can avoid on your path to networking success.

Networking doesn’t necessarily mean you need to go out and actively pursue new relationships right away. Instead, start with cultivating and investing in the relationships you already have. There is a lot of power in the contacts of your contacts

Consider networking like a puzzle. As you piece the puzzle together, you might have gaps that need to be filled. Take a look at your current resources and see how you can use them to fill that gap.

You never know when you’ll need someone to help connect you. However, it’s not a good practice to ask someone to do something for you when you haven’t spoken with them in a while. In order to avoid this awkward situation, make it a point to keep in touch with your contacts.

Create “reconnect” files in your calendar to stay organized by establishing lists of people you are connected to and need to keep in touch with on a monthly rotation. Designate contacts that have obvious networking potential, and connect with them on a monthly basis.

Connecting is as easy as sharing interesting articles. When you don’t lose touch with your contacts, it’s easier going to them with a networking request.

LinkedIn is a great tool to use to make virtual connections. Find your existing contacts on the platform and link to them. Then, take a look at their contacts to see if they have any networking opportunities that could help you. If you see someone, ask for an introduction.

Networking isn’t all about taking; you need to give a little without expecting something in return. It’s obvious if you’re only focused on your own gain, but it’s also obvious if you’re being genuine, so follow these tips to make yourself a contact people want to have.

Face-to-face networking is vital, but social media networking is still useful. It’s a great tool to use to open the door to hundreds of new contacts, but social media sites should be used wisely. Check out these tips for networking on social media.

Get a little boost in growing your online network by following these three phases.

1. Comment and Retweet

Leave a short comment on blog posts from organizations and people you want to connect with. It can be as basic as saying, “Great post, I learned something new,” and retweeting the article to your Twitter.

2. Amp Up Phase One

Add some depth and meaning to your comments, and make your retweets appealing enough that other people want to check out the content. This will help you make more contacts, too.

3. Mention Others

In your own content, start to mention other contacts just as much as you mention yourself. As you promote your contacts, your relationship with them grows, and everybody gains from it.

TAKEAWAY

While you might go into networking for your startup with the mindset that you’re doing it for your own gain, you’ll quickly realize that networking is largely dependent on the give and take. Just like any personal relationship, your networking connections are all about creating value for each other to remain healthy and beneficial to everyone. As you learn to give to others and focus on them, you’ll find that your connections will give back to you.

(!!) And, the most genuine way of showing virtual appreciation for a writer is to share & tweet. In case you haven’t done it yet … I’m looking forward to it! Thank you for reading/watching this and stay tuned for next week’s post.

By Tommaso Di Bartolo at What It Takes, for The Pitch

“What is the burn rate for your company?” … Can you answer the question? If you can, is your answer accurate? If you don’t know the answer, or you don’t know if your answer is the right one, you better learn how to determine the right level of burn rate for your startup.

A startup I recently was introduced to was in panic mode when they hit the point of having only enough money to operate for three more months. As they frantically tried to raise funds, we went into their burn rate and was super surprised when they told me “they didn’t know for sure” what it was. While they had an estimate when they started, they were using the money for things like frequent travel and comped meals, and they didn’t figure those costs in their burn rate.

To make a long story short, I helped them leverage a Syndication investment to raise a bridge round and keep operating. With that experience under their belt, they got serious about determining the proper burn rate for their startup and not to neglect their burn rate anymore. As a consequence of that situation before raising funds, they became confident about the amount of burn money they had in the bank, and they had less instances of panicking for funds thanks to determining the right level of burn rate for their startup.

Getting Personal with Your Burn Rate

Realistically, you won’t be able to come up with an exact number for your startup’s burn rate. It is a very personal issue and will vary between startups, so there is no universal answer. You need to decide for yourself what yours is. While you won’t get a specific answer, you’ll want to be pretty accurate and not too high so you know how much runway you have until you need to raise more money. Use the following to figure out an estimated burn rate for your startup.

There’s no right or wrong answer, it’s just vital to know your risk tolerance.

Use the Formula

Depending on where the startup is located, you can figure $10-12k times the number of employees. For example, if your startup is located in an area that has a higher cost of living, like in Silicon Valley, your startup’s burn rate will be higher than a startup in a midwest location.

This can vary based on the type of company. Consumer companies tend to go through more cash in their early years compared to SaaS companies. Consumer companies don’t see revenue until their consumer adoption has reached a larger scale. The average consumer public startup doesn’t exceed a $1 million monthly burn rate at any point. Alternatively, SaaS companies will burn about $1.5 million as they scale up, but once they go public, their burn rate will fall to sub-$1 million per month.

Why Knowing is Important

Having a lower burn rate allows you to go longer without having to raise more cash. While raising funds is an ongoing job duty for startups, if you can manage your burn rate, you can spend less time on raising funds. Also, the frequency in which you have to raise funds can decrease, which allows you to focus on other areas of your startup.

Do you have a product/market fit that requires an aggressive burn rate. Without a true product/market fit, there is no sense in increasing your burn rate aggressively to stimulate your future growth. For SaaS businesses, you need to monitor indicators like MRR growth, churn rate, cost of customer acquisition, and payback period. The model may be different for consumer startups. You may need to monitor usage and engagement. It will be unique for each startup, depending on the company type.

Are you scaling up hiring for the right reasons? Startups may feel the need to scale up and get the best employees, developers, engineers, etc. because they believe the startup game is an arms race. However, when you have limited funds and a burn rate you need to stick to, you need to consider hiring only when you have a real need for more bodies in your startup.

Are you spending more than 5% of your budget on things besides payroll, benefits, and rent? Of course, you need to spend in the areas listed as they are essential to making your startup work. However, things like servers, advertising, meals, and travel are easy to overspend on, and it’s a good place to look if you are going through your burn rate faster than you should be.

Are you willing to do what is required to break even? It’s not an easy decision, but it might be necessary to let some of your workers go, reduce salaries, eliminate certain salaries, sell some of your extra office equipment and other things, downgrade to a more affordable office or apartment, or even relocate to a cheaper city.

A venture-backed path requires putting a lot of stress on a new business. Be ready to do things that normal businesses don’t have to do when you are on a venture-backed path. You are expected to tackle a big-money opportunity and achieve hyper growth year-over-year. Be ready to put a lot of stress on your startup to grow quickly and take the market as fast as you can, because if you don’t, someone else will. You need a market that is big enough with a large and undeniable target to where your startup will be able to take a small part of it.

TAKEAWAY

As a startup, your budget is a huge part of your future success. It’s important to determine what burn rate is right for your startup so you can make it to your milestones without running out of money. When you’ve determined the right burn rate, you can work on scaling up. Open communication with your investors is key, as is taking a hard look at where you are spending your funds.

(!!) And, the most genuine way of showing virtual appreciation for a writer is to share & tweet. In case you haven’t done it yet … I’m looking forward to it! Thank you for reading/watching this and stay tuned for next week’s post.

Have you been experiencing failures in your startup? If you have, you’re not alone. Most successful startups and entrepreneurs experience failure at some point in their lives and careers. What distinguishes those who are successful and those who are not is how failure is handled. In order to find success, failure needs to be embraced. By changing your perspective on failure and how you handle it when it inevitably comes your way, you can learn a lot and find success quicker.

Q4 last year I worked with a startup that had two leaders. Both of them were incredibly passionate about the project, and they truly believed they had something special. Within six months however, it became clear that their startup was going to fail. It wasn’t for a lack of trying, it just wasn’t the right product for the market. In this instance, it wasn’t the failing that was the issue, it was how the leaders handled it.

One of them was ready to learn from their mistakes and move on. She was optimistic about future success in spite of their current situation, and she believed that they needed to focus their attention and time on a completely different aspect of their startup. While she was upset for couple weeks, she quickly moved on and was ready to move forward.

However, the second leader was not in the same boat. He was worried that their failure would ruin their reputation, and he felt that their best bet was to try to make the original project work and not give up on it. His frustration and passion got the best of him, and in the end, he couldn’t let go of the original project. The two leaders ended up parting ways, with the first eventually finding her way to success.

Accepting Failure

No matter how hard you work and how passionate you are, failure is in many cases going to happen. Working on a startup, you need to understand that failure is likely and normal, and it can be looked at as a positive learning. Failure can be a good thing if you understand that you got much closer to success. Follow these steps to accept your failure and move on.

Learning and Moving Forward

90% of startups fail, but great startups can turn their failures into lessons and move on successfully. How you deal with your failure will determine how successful you will be, and it says a lot about you as an individual.

One essential lesson is to fail more quickly. If you are stuck in a bad idea, don’t keep trying to make it work. Move through it to arrive at great ideas that will allow you to be successful and propel you forward. Don’t make the same mistake twice.

As the saying goes, when one door closes, another one opens. The key is to not focus too long on the closed door, and look forward to the open one. Brainstorm new ideas, research ways to be successful, and don’t let your failures steal your motivation.

Changing Your Attitude about Failure

Our society tells us failure is bad. We hate to fail, and some people may even live in fear of failure. When failure happens, as it inevitably does, many people tend to cling to it and allow it to control their emotions. Some people may even stop trying altogether in order to avoid failure. As a startup, failures need to be embraced, as they are likely to happen. Consider these ways to change your attitude about failure.

You’re in Good Company

You will be hard-pressed to find a success story, either from the past or current day, that hasn’t failed at some point in their lives and careers. Those who have distinguished themselves by their successes are likely to tell you that failing was critical to their achievements. Failure was likely their motivator, and they learned from their failures. They used failure as a stepping stone to success and never gave up. Here are some examples of famous failures.

TAKEAWAY

Even the greatest minds of history and of our time have experienced failure in their lives. Most of them failed multiple times, so as a startup, you shouldn’t be too surprised when you fail, or dwell on it too much. If you have the right perspective and learn from your failure, it can be used as a stepping stone to your eventual startup success.

(!!) And, the most genuine way of showing virtual appreciation for a writer is to share & tweet. In case you haven’t done it yet … I’m looking forward to it! Thank you for reading/watching this and stay tuned for next week’s post.

Raising funds for your startup is like a second full-time job on top of developing your startup. It usually is stressful, nerve-wracking, and often confusing. How do you know what investors want to hear? How do you know what to include in your pitch and what to lead out? And, most importantly, how do you know what will catch investors’ attentions?

When I was preparing for the F50 Investor Demo Day back in 2014, I was not only eager to hook the 200+ attending investors, but I was also looking to find a way on how to grab the audience attention and be remarkable - rather than become another startup pitch. It took me over 10 days to prepare the keynote including its structure, design and to practice the pitch. In order to get to 120 seconds speech - I wrote first a story of a couple pages, reduced it than to the core message I wanted to convey per slide and transformed it then into a story to make the audience navigate through the business case. On the night before getting on stage - basically ready to rock - I was having dinner with my family when I still had the feeling that the pitch could be more unique, when I turned to my older son David (13 back than) and asked if he’d be open to jumping on stage with me and make a short entertaining intro to grab the audience’s attention. The product I was pitching back then was an app for teens - so it would come across amazingly well for David to make an opening.

Because David loves acting - it was an easy one for him to learn the “story on how the idea come up - and why this became the reason for me (his Dad) to solve this problem”. It was an amazing experience and the audience was not only excited during the presentation but had huge responses also after the pitch.

Honey Your Core Value Proposition

Your pitch isn’t just what you’ll share on demo day. Your startup’s pitch embodies the core message that you’ve honeyed with peers, family, friends, mentors, and employees over and over again. It’s the first impression of how your idea will make the world a better place. Your potential investors will decide in the first minute whether or not they are interested, so show them you are credible and tell them what problem you are solving and why they should care right off of the bat. Preparing a pitch that’s to-the-point and easy to understand will be useful every time you need to explain your startup and its purpose.

Less is More

The quickest way to turn off an investor is to drag your presentation on and on, give lengthy explanations, and have too much information on your slides. Don’t save the “good stuff” for the end. Hook the audience within the first couple of seconds and be succinct and thorough in your presentation. You need to craft an elevator pitch to catch investors’ attentions and impress them. Keep everything short, sweet, and to the point, so investors can see that you will be able to attract and keep customers.

Follow the K.I.S.S. Method

Albert Einstein once said that if you can’t explain something simply, you don’t understand it well enough. The same goes for your startup. You should know it better than anyone, since it is your creation, but if you are unable to simply describe your startup, then you don’t know it well enough. Go back and reevaluate what exactly your purpose is. This guideline goes hand-in-hand with the less is more idea. If your investors can’t grasp your concept quickly, they will assume that potential customers won’t understand it, either. It will be hard to get funding if investors don’t know what they are giving their money to.

Practice, Practice, Practice

You only have one shot to get it right, so practice your pitch multiple times before meeting with investors. Practice in the bathroom in front of the mirror, give your pitch to family and friends or a mentor who will give you honest feedback, practice when you’re driving in the car. Feeling comfortable with your pitch will help you relax and seem more natural during the presentation. Investors are typically good judges of character, so they will be able to see through you if you aren’t being natural or aren’t comfortable with what you are pitching.

Talk traction

Investors are more likely to give money to a sure thing, not a startup who has no data to back up their projections. Show that you are a low-risk investment by showing some traction and real-world experience in your pitch, and you’ll be much more likely to raise money than if you were just to forecast returns. If you don’t have the ability to do a full launch, find a way to test your startup’s viability and product on a tight budget. Show that your idea is needed before pitching it to investors.

Be Unique

Investors will compare your pitch to others that they have heard, so it is important to make your presentation stand out from the crowd. Ask yourself these two questions:

- What elements are unique to your business?

- How can you best display those elements?

Incorporating a little bit of humor, an interesting story, or just overwhelming proof of the viability of your startup will help to set you apart, as well. There are many little ways to be appropriately different and catch an investor’s attention.

Be Credible and Confident

It’s important to be honest with yourself and realistic about what you need from investors. Take a hard look at how much money you actually need so you don’t scare away investors with a huge number, and don’t bite off more than you can chew. Demonstrate that your startup can crawl before it can walk. Perfect your tactics for a single product before you try to launch 50. Read your pitch and ask yourself what it says about your business. Rewrite it until it says what you want to convey.

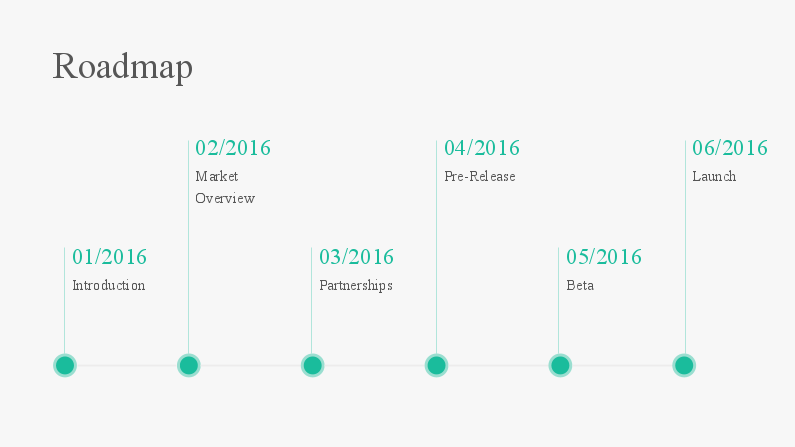

The first minute of your pitch is critical. Either investors are going to pay attention or tune out. How do you hook them? Having a compelling deck that touches on the 12 points below is important to success when raising funds.

Slide One: The Hook

This slide is your hook, and it will vary based on the entrepreneur type and business stage. Start with statements that compel the investor to listen. The goal of slide one is to catch their attention and have them say, “This sounds interesting.”

Beyond your elevator pitch follows the strongest argument that makes the investor keep on listening. Investors hear pitch after pitch, so the sooner the “wow” moment appears, the better. To get that attention-grabbing moment, answer one of the following questions right away. Select the one that best supports your startup and makes the strongest case for you. The list is in priority order.

1. What have you already achieved? (Traction)

Answer this question with traction numbers or money raised.

2. What have you done in the past that makes you an impressive founder or team member? (People)

3. Why are you pitching your product today? (Purpose)

Tell the story what happened / motivates you / why you are doing what you are doing.

Slide Two: 50,000 Foot View of Your Company

Give investors the big picture view of what you are doing, and get them excited about the potential. Make sure you convey your passion behind the scene using a punchline. Focus on the value proposition.

Slide Three: Unmet Need

Your investors are going to wonder what problem your startup is going to solve. You will need to make clear that there is a need only your startup can meet. Or, if the need is already being met, explain how you can meet it faster, easier, and better. Show how it’s done today - and explain why it’s broken. The best way to do so is to tell a story.

Slide Four: The Solution

Now it’s time to present how you solve the customer’s pain! Showing your product is essential to a pitch. If it is not complete, then show a mock-up. If it is a service, show how it works. Investors are more likely to fund you if they see and understand how your product solves the need you described. A visual representation of your product can have a big positive impact on the overall effectiveness of your pitch. Transition into a product demo or user story by saying something like, “Let me show you how this works.”

Slide Five: Market Sizing

Now that you’ve got investors excited with your solution to a need, and they’ve seen how it works, it’s time to tell them how big it can get. It’s important to put some effort into researching the answer to this question. One way to do it is through bottom-up market sizing. You take the number of potential customers and the price of the product sold. So, if you have 100 potential customers for a $20 product, the market is $2000.

There are some market sizing pitfalls to avoid:

- Using a large number a small market share to make your startup seem like a sure thing.

- Giving “conservative estimates” that are unlikely to be met.

Slide Six: Go-To-Market

How do you take your product to market? What are the main traction channels, partnerships that leverage you into your target audience? Describe how you’ll reach your first 10 - 100 - 1000 users/customers.

Slide Seven: Competition

Never say that you don’t have any competition. Even if it is indirect, it is still competition. Worst case - the way that it’s done today (behavioral) is your competitor. Address your competition and what differentiates use using a matrix format so it is easy to see in what areas you outdo the competitors.

Slide Eight: Traction & Customer Adoption

The key performance indicator (KPI) that you are measured on will define what your product stands for. Don’t choose something too general like downloads or revenue. Instead, show an AARRR funnel perspective to give investors a clear idea of how your product is gaining traction throughout the funnel.

Slide Nine: Financial Projections

Keep your projections realistic and avoid hockey stick projections. Investors won’t take you seriously if you show an unrealistic growth over a short amount of time. Show them that you are realistic in your projections.

Slide Ten: Team

Investors want to know that you have a strong team to back you up. Bios will need to be relevant to someone who will be given you money. Don’t focus too much on the team’s accomplishments, but keep it relevant and include photos. Let investors know that they are experienced and have the expertise.

Slide Eleven: Roadmap / Timeline

Show investors that you will be smart in investing the money you raise, and give them your investment plans. Show a graph which reflects how much Dollars you need to get to what milestone. Include quarterly dates and eventually how your team will grow.

Slide Twelve: The Ask

End with what do you need to keep your company going. This includes but is not limited to Investment money, Customers, Partnerships, Advice. In the case of fundraising, let investors know when you are closing the round.

Appendix: Backup Slides

Murphy’s law states that anything that can go wrong will, so you should always have a backup plan for your slides. This is especially true for tech startups. Keep a backup on a thumb drive, bring an AC adaptor and extension cord for your laptop, and have an extra laptop on hand just in case.

TAKEAWAY

Every pitch is different. Are you having a 1:1 or a 1:many. Is it a 2-minute pitch or an investment firm partner meeting! Develop a custom template touching the twelve POINTS above (NOT twelve slides) you can adjust accordingly. Emphasis your strength and you passion and never beg. Telling a story will make the problem and it’s solution much more tangible. Build a “story arc”: start with a bang - and end with sympathy and agreement!

(!!) And, the most genuine way of showing virtual appreciation for a writer is to share & tweet. In case you haven’t done it yet … I’m looking forward to it! Thank you for reading/watching this and stay tuned for next week’s post.

Do you feel like you’ve exhausted and struck out with the entire available employee pool in Silicon Valley and still have vacant positions at your startup? Maybe you can’t find someone to fill the exact need you have, or maybe the wage demands are impossible for you to meet at this point in your startup. Of course, you’d love to pay your employees what they want, but that’s not always possible in the early stages of your company. What do you do when you’ve run out of local options? If you’re in this position, it’s time to expand your talent search and consider hiring remote workers. But how to broaden your scope?

A startup I recently worked with had a serious challenge that many companies, new and established, face. They were having a difficult time finding quality employees with experience and talent that fit into their payroll budget. In Silicon Valley - as in every other Tech hub around the globe, affordable talent is hard to come by, especially for startups. The founders couldn’t sacrifice anyone else’s income, and they also didn’t want to end up with sub-par employees just to fit into their budget.

As a solution, I suggested that they “act” outside of the box by decentralizing the team. In this case, the box was perceived geographic restraints. Instead, they investigated hiring remote workers to fill their vacancies. Many jobs, especially in the tech industry, don’t really need workers to be in an office space to fulfill the duties. While the startup was worried about managing remote employees, they decided to take the plunge. What they found was a larger talent pool at a more affordable price, which was exactly what they needed to continue moving forward with their startup. They were delighted to discover that an engineer from Wisconsin or a designer from Texas was just as talented as the candidates they were considering in Silicon Valley. With their positions filled, they were able to make excellent progress moving forward towards success with their startup.

Why Remote Workers Love Joining (Silicon Valley) Startups

There are many more benefits than what’s listed, but these are some of the more compelling reasons why you should hire remote workers.

1. They can’t move to you or away from you

Many people are tied down by a mortgage, kids in school, or a spouse with a great job. They would love to move to Silicon Valley and work for you, but they can’t. However, by hiring remotely, you are opening up your search to hundreds of people who have great experience that you might have missed out on just because of where they live.

An in-office employee moving away has a big impact on both your work culture and your productivity. There are so many reasons why someone would leave a job, and many of them have to do with geographic location. You won’t lose anyone due to needing to be closer to family, leaving because their spouse got transferred or is attending school somewhere, or not being able to afford living in Silicon Valley anymore. When a remote worker moves, the most you need to sacrifice is maybe a few days of vacation to make the move. Otherwise, since they can work from anywhere, you can rely on them as permanent employees.

2. There are plenty of fish in the sea

For every one employee who is in your location and could work for your, there are at least 100 more who are not. Restricting your accessible talent pool to your geographic area removes hundreds of quality workers from your search. If you’re creating a tech startup in an area that isn’t tech-centric, hiring remotely would allow you to find developers, coders, or engineers in places like San Francisco and Boston. You can even make your search worldwide to the enormous pool of talented workers from anywhere like the Philippines or France.

3. Remote workers are more productive

You might be inclined to think that remote workers would spend less time worker than their in-office counterparts, but the opposite is actually true. In fact, in a recent survey by Global Workplace Analytics, 53% of remote workers reported that they were likely to work overtime, compared to only 28% of in-office employees. With the flexible hours and no commute that remote working allows, it’s easy to see how they wouldn’t mind working an extra hour or two every day.

Offices are full of distractions. From impromptu meetings to chatty colleagues, there is plenty happening that can take you away from your work. At home, your workers can focus on their tasks completely uninterrupted. Additionally, office hours are typically set from nine to five, and not everyone is at their most productive during that time. You might have employees that get the most done when everyone else is asleep, or like to bang out their tasks before the sun comes up.

Additionally, office workers often equate being at the office as working. It’s impossible to know how many hours your employees are actually working while they are at work, so you need to gauge productivity by what is getting done. Remote workers can’t fool themselves into thinking that they are “working” by just sitting at their home computer, so they tend to be more productive during their work hours.

4. Communication improves

When you first start out, the few employees you have know everything. As you grow, it’s impossible to keep that up without top-notch communication, and you can’t rely on overheard conversations of water cooler chats to spread information. You have to work with different channels like Google hangouts, Slack and other type of communication and collaboration platforms to stay in touch.

5. Find more qualified workers

Restricting your search to one area or demanding new hires to relocate can dramatically narrow your results. By hiring remote employees, you broaden the talent pool and include a larger number of qualified workers in your search. As an added bonus, remote workers tend to be happier than in-office workers, which can translate into better results.

6. Remote workers save you money

As a startup, one of your biggest concerns is budget, and replacing an employee is a cost that you might not be able to handle. It is estimated that an employee making $50,000 per year will cost you 20% of the salary to replace. If any of your positions require high levels of training or education, the turnover cost will be even higher. Remote work can be used as a perk to retain your best workers and avoid having to pay to replace in-office workers.

Recruiting new employees can cost you $7000 on average, or possibly more if you use a recruiter. That’s a big chunk of change for startups, and you might not even be happy with who the recruitment agency selects for you.

The time it takes to hire someone averages 10 to 12 weeks from job posting to an accepted offer. All of that downtime means there is either no productivity or the job is being diverted to someone else, which is going to cost you money, too.

Not having to rent a big office space allows you to save money as well. In fact, a recent study found that switching to telecommuting full time could save your business $10,000 per employee per year in real estate costs. For a startup, that is a huge savings. Utilizing remote workers helps you avoid expenses that on-location working requires like office chairs, office supplies, janitorial services, and utilities.

Finally, remote workers are less likely to call in sick or miss work due to inclement weather. Unscheduled absences like these can cost your startup up to $1800 per employee per year.

7. Scale as you grow

What happens when you outgrow your current workspace? Moving an in-house team every year or so is expensive, time-consuming, and labor-intensive. With a remote team, you’ll never have to move offices, and your employees can function in a convenient way.

Things to consider before going remote

Remote work has plenty of benefits, but there are a small number of challenges to consider, too.

1. Your management style will need to adjust

Managing a team of professionals in different locations is not the same a managing an in-house team. You’ll want to make it a point to reach out to each of your remote workers on a regular basis and make an extra effort to stay connected to them so they feel like they are part of the company’s culture. Investing time in your remote workers will make them feel like they are truly part of the team, and they are likely to stay loyal to you, too.

You will want to be as transparent with your remote workers as you are with your in-house ones, and give them the same access to information as everyone else. There are different tools like Dropbox and Gdrive that allow you to share information easily.

2. Not everyone is cut out for remote work

Not everyone will find the freedom of remote work a way to become more productive. The ability to hire the right people for remote work is key. Certain personality traits and values align well with remote work, and you should look for those things. People who are self-motivated, organized, good and managing time and priorities, and can work independently are ideal candidates for remote work.

Since much of the communication done with remote workers is via chat or email, you’ll want them to be good writers. A bad writer can turn a short chat into a long one, which cuts into valuable time and decreases productivity. Find some way to test writing skills in the interview process to weed out the applicants who can’t write clearly and concisely about complex issues.

If you are interviewing someone who has not worked remotely before, be sure to thoroughly cover all of the concerns, questions, and possible issues in the interview so there are no surprises once they start working.

3. Hiring will still take some work

Although you’re increasing the talent pool you have to work with, it still might take some effort to attract qualified applicants. You may need to spend some time actively recruiting people to apply for positions with you. To find qualified workers, go to job boards where your ideal candidates are likely spending their time. Posting on the big sites like Monster or CareerBuilder for a specific and highly-skilled position isn’t a good idea. AngelList is a good resource for startups to use to find remote workers, and other resources are WeWorkRemotely, Dribbble, and SupportOps.

Check also Hubstaff‘s Infographic on “The 9 Step Process To Manage Your Remote Team”.

Tools for remote workers and employers

In addition to the job boards mentioned above, popular services like Freelancer.com, PeoplePerHour, and Upwork allow startups to find affordable remote workers to complete small tasks or work on specific projects.

Sophisticated freelancer management systems are emerging for startups to make it easier to manage remote workers. These systems help create a digital bridge between full-time employees and remote workers to help everyone stay integrated and connected.

For communication, things like HipChat, Grape, Google Hangouts and Skype for Business allows you to make face-to-face contact with your remote workers on a regular basis. Having a great human resources information system and some type of shared drive is invaluable with remote employees. Software that allows simultaneous, multi-user editing and collaboration is necessary if you’re using remote workers.

TAKEAWAY

Startups can benefit in a number of ways when they take advantage of remote workers. Not only does it open up a large and talented workforce that you might not have access to locally, it allows you to save money and scale as you grow. Find the right marketplaces for your niche and execute on it.

(!!) And, the most genuine way of showing virtual appreciation for a writer is to share & tweet. In case you haven’t done it yet … I’m looking forward to it! Thank you for reading/watching this and stay tuned for next week’s post.

According to Juliet (Shakespeare, Romeo and Juliet), a name should mean nothing, but for a startup, it’s a completely different story. Choosing a name for your startup can be one of the most important decisions you make in the beginning, and for a good reason: it is the most impactful choices you’ll take. That’s why it is pretty common, that startups before getting product-market fit change their names a couple times. Unfortunately, not every startup gets enough time and they realize too late that they chose a lame name. But what is in a name?

I’m passionate about finding names that make people connect with the brand. MailplusWeb - was a cloud security vendor focused on email and web security. With Cloudplace, I created a white labeled storefront for Enterprises and Telcos - for them to have “one place - for all cloud services”. Swaaag was a mobile social video app, born to take teens beyond the like (before Snapchat became what it is today)… or my latest gig called corpor8.fm an Invitation-Only Channel for Corporate CxOs to discuss Innovation in disrupted industries. And this, just to mention couple companies of mine in the past.

In a mentor session 8 weeks ago I helped a startup that seemed to be doing a lot right, but they couldn’t get their ecosystem hooked, nor get any brand recognition and interest from investors. They were active on social media, they put themselves out there as much as possible, and they were rolling out pretty smart go-to-market tactics to gain users. When we first spoke, I liked the problem they solved - but the name they chose sucked.